In the realm of financial management, the impact of activity-based costing (ABC) on overhead cost allocation and cost management cannot be overstated. The ABC system provides a more accurate approach to assigning indirect costs to products and services than traditional costing methods do, thus improving cost efficiency and driving better decision-making. This article will explore the nuts and bolts of ABC, providing an in-depth understanding of this critical financial management tool. You can also discover more about our activity-based costing software solution.

Key Takeaways

- ABC focuses on allocating overhead and indirect costs based on causal relationships between costs, activities, and outputs.

- Activity-based costing is especially beneficial to the manufacturing industry due to the complex nature of the production processes.

- Cost drivers, which can be transaction or duration in nature, serve as the foundation for ABC’s granular approach.

- ABC influences pricing strategy formulation, which can provide a competitive advantage to businesses using it.

- Despite offering increased accuracy in overhead cost allocation, ABC has its challenges, such as inherent complexity and potential inaccuracies.

Understanding ABC Activity Based Costing

Activity-Based Costing (ABC) has emerged as an improvement to the traditional cost accounting system, offering advantages in the allocation of manufacturing overhead costs by focusing on the activities responsible for incurring these costs. To understand the full benefits of ABC, it is important to delve into its inception, development, and core principles.

The Genesis and Evolution of Activity-Based Costing

ABC was developed as a response to the shortcomings of traditional cost accounting systems, which typically allocated manufacturing overhead costs based on machine hours, leading to distorted and inaccurate cost representations. Companies with high overhead costs that did not directly correlate with production volumes, or those offering diverse product ranges and accommodating varying customer demands, necessitated a better approach to indirect cost allocation. As a result, the concept of ABC was born with the goal of providing a more accurate and logical foundation for assigning costs to activities that consume resources. Click here to download a detailed case study on how ABC is implemented today.

Defining Activity-Based Costing (ABC)

- Cost Accounting: ABC advances conventional cost accounting by allocating indirect costs based on the actual activities causing costs, rather than on arbitrary factors like machine hours.

- ABC inception: The advent of ABC reflects a focus on accurate cost representation and a departure from the inadequacies of traditional costing systems, driven by the evolving business landscape and resource-intensive production processes.

- Manufacturing Overhead Costs: ABC apportions manufacturing overhead costs to products based on the specific activities and resources they require, resulting in a more precise indirect cost allocation.

- Indirect Cost Allocation: By attributing costs to activities that consume resources, ABC disperses indirect costs more logically and accurately than traditional methods, leading to a clearer understanding of a product’s true cost structure.

By concentrating on the causal relationships between costs, activities, and outputs, ABC offers an effective method for aligning resources with their respective cost drivers while providing invaluable insights to drive informed decision-making and financial management strategies.

Core Principles of ABC Activity Based Costing

At the heart of the ABC method lies the concept of activities serving as cost drivers. Cost drivers are events or units of work that have specific goals or objectives, such as machine setups or processing purchase orders. By understanding the activities that drive costs, businesses can allocate overhead costs more accurately and ultimately make better-informed financial decisions.

ABC relies on two distinct types of activity measures: transaction drivers and duration drivers. Transaction drivers measure the number of times an activity occurs, while duration drivers record the time taken to complete the activity. By employing these two measures, ABC moves away from traditional volume-based cost allocation methods and more accurately links indirect costs to varying levels of activity required by different products or services.

- Transaction drivers: These measure the frequency of activities and help businesses understand the number of times a specific cost driver occurs. Some common examples of transaction drivers include the number of machine setups and the number of purchase orders processed.

- Duration drivers: These measure the length of time an activity takes to complete and assist in calculating the efficiency of a specific cost driver. Examples of duration drivers include the time spent on machine maintenance or the time required for a quality inspection.

By focusing on activities and their corresponding cost drivers, ABC enables a more accurate overhead cost analysis and a more direct cost allocation method. This helps businesses better understand the true costs of their products and services, facilitating more informed decision-making and strategic planning.

Activity-Based Costing in Action: A Scenario

Now that we have understood the basic principles of Activity-Based Costing (ABC), let’s explore its application with a practical costing scenario. This will provide valuable insights into the process of cost drivers identification and how a comprehensive costing analysis can be performed using ABC.

Identifying Cost Drivers in ABC

Imagine a manufacturing company that incurs a significant electricity bill, mainly due to labor hours. In this case, labor hours become the cost drivers, as they directly impact the total electric bill. With the ABC method, cost drivers are identified to allocate costs accurately, enabling businesses to pinpoint the source of their overhead expenses. Now that we have understood the basic principles of Activity-Based Costing (ABC), let’s explore its application with a practical costing scenario. Request a Demo.

Examples of Calculating Costs with ABC

To demonstrate the allocation of costs using ABC, let’s consider a scenario where the company has three major cost drivers: machine setup, labor hours, and utilities (electricity and water). The first step involves creating a table to organize the cost pools and cost drivers associated with each.

Cost Pool | Overhead Cost | Cost Driver |

|---|---|---|

Machine Setup | $20,000 | Number of setups |

Labor Hours | $30,000 | Wage hours |

Utilities | $10,000 | kWh and Liters |

With the cost pools and drivers in place, the next step is to calculate the cost driver rates for each cost pool. This can be done by dividing the total overhead cost of each cost pool by the total number of cost drivers. These rates allow for cost allocation to products based on the resources they consume.

- Machine Setup: $20,000 / 200 setups = $100 per setup

- Labor Hours: $30,000 / 2,000 hours = $15 per wage hour

- Utilities: $10,000 / 5,000 kWh = $2 per kWh and $10,000 / 2,000 Liters = $5 per Liter

Finally, we can utilize these cost driver rates to allocate costs to each product based on the resources they use. This comprehensive costing analysis can help businesses identify where their costs are coming from and optimize their manufacturing process accordingly.

This overview introduces the core mechanics of ABC, but the real-world corporate cost allocations are more complex. Our corporate cost allocations whitepaper shows how leading organizations apply ABC at scale. Download the whitepaper to move from theory to practical entprise cost allocation.

Calculating Costs: The ABC Activity Based Costing Formula

Implementing the activity-based costing formula to calculate overhead costs and allocate indirect costs can significantly contribute to a company’s financial management strategy. The process involves several stages that lead to a more transparent and accurate understanding of product costs.

- Identify and categorize the activities required for product creation into cost pools with specific overhead costs.

- Link cost drivers to each cost pool.

- Divide the total overhead cost of each cost pool by the total cost drivers to determine the cost driver rate.

- Multiply the cost driver rate by the amount of the cost driver utilized to allocate costs to products. Learn how to maximize value from the ABC calculation.

Once these steps are completed, a nuanced view of product costs based on real resource usage is achieved. This detailed costing methodology ensures that your organization can make more informed decisions in cost reduction and revenue optimization.

For instance, let’s examine an example calculation of overhead costs in a manufacturing company:

Cost Pool | Overhead Cost (USD) | Cost Driver | Total Cost Drivers | Cost Driver Rate (USD per driver) |

|---|---|---|---|---|

Machine Setup | 10,000 | Number of Setup Hours | 200 | 50 |

Inspection | 8,000 | Number of Inspections | 80 | 100 |

Packaging | 5,000 | Number of Packages | 5000 | 1 |

In this example, the total overhead costs are allocated based on the cost drivers specific to each cost pool. Using these cost driver rates, an accurate indirect costs calculation can be carried out to properly allocate overhead costs to each product, giving you a better understanding of the profitability of each product line and how to optimize your organization’s activities.

The Impact of ABC Activity Based Costing on Business Strategy

ABC activity-based costing plays a significant role in shaping business strategy, primarily through its influence on pricing and decision-making. By offering a detailed understanding of product costs, ABC enables companies to make strategic pricing and cost management decisions based on true value and resource allocation, ultimately unlocking competitive advantages.

ABC’s Role in Pricing Strategy

Strategic pricing is paramount for any business seeking to ensure profitability and long-term success. ABC provides accurate and granular product cost insights, enabling organizations to establish pricing strategies that reflect the true value of their offerings. With a comprehensive understanding of the costs associated with activities and resources, companies can identify where improvements can be made to enhance product profitability or pursue alternative pricing models that better align with their cost structures.

Using ABC for Competitive Advantage

Leveraging the insights gained from ABC, businesses can craft competitive pricing strategies that take into account both their operational efficiencies and market dynamics. By employing a cost management strategy that encompasses an in-depth analysis of cost pools and cost drivers, organizations can pinpoint areas where they can streamline operations, reduce costs, and improve margins. As a result, businesses can achieve a competitive edge, utilizing their newfound knowledge to make informed decisions about product offerings, customer targeting, and market positioning.

Advantages and Limitations of ABC Activity Based Costing

Activity-based costing (ABC) offers several benefits to organizations while also presenting certain limitations. These advantages and challenges arise primarily from its focus on accurate costing, detailed overheads analysis, and the cost allocation methodology it employs. Understanding these aspects is crucial for organizations looking to utilize or improve their ABC costing system.

Enhanced Accuracy in Cost Allocation

One of the prominent benefits of ABC is the increased accuracy in the allocation of indirect costs. This refined approach assigns overheads to an expanded number of cost pools and utilizes new bases for cost allocation. As a result, indirect costs become more attributable to specific activities. By design, ABC fosters more precise cost allocation, providing better insights into the relationships between overhead costs and the activities causing them. This increased accuracy is particularly valuable for organizations with substantial indirect costs that differ significantly across diverse product lines or service offerings, as it allows for more informed decision-making in areas such as pricing or process improvement.

Challenges and Critiques of ABC

Despite the benefits of employing an ABC system, the methodology presents some challenges. One of the key critiques often leveled against ABC is the complexity inherent in implementing and maintaining the system. The process of identifying the relevant cost pools and cost drivers, as well as their relationships and values, requires significant resources and expertise, which may pose a barrier for smaller businesses or those with limited resources.

Another challenge lies in the potential for inaccuracies if cost drivers are not correctly identified or applied. This can lead to distorted cost allocations that do not accurately represent the underlying cost structures and causations. Such inaccuracies can have wide-ranging implications, potentially affecting product profitability assessments, operational efficiency evaluations, and overall business strategy development.

In conclusion, while ABC offers numerous advantages for organizations looking to enhance their cost allocation and overheads analysis capabilities, these benefits must be weighed against the challenges posed by its implementation and maintenance. Companies considering adopting an ABC system should carefully assess the trade-offs involved and consult with experienced professionals to optimize the approach for their unique circumstances.

ABC Activity Based Costing Definition

ABC (Activity-Based Costing) is a method for breaking down the costs associated with products and services, providing a detailed understanding of the underlying cost drivers and their effects on business finance. To better grasp this concept, it is crucial to recognize the essential ABC terminologies and the process through which it delivers precision in cost management.

Breaking Down the ABC Terminology

Two primary terms are involved in ABC:

- Cost Pools – These are groupings of individual costs connected to specific activities or processes. By accumulating and segregating these costs, it becomes easier to understand the relationship between activities and the overhead costs they generate.

- Cost Drivers – Factors that create costs, such as machine setups or quality inspections, are referred to as cost drivers. They provide essential insights into how resources are utilized in the production process and help in allocating overhead costs based on their actual consumption.

The Detailed Explanation of ABC

The ABC methodology involves calculating the cost driver rate by relating total overhead costs to the number of occurrences of the cost-driving activity. With this cost driver rate, businesses can determine how much of each overhead cost can be allocated to a specific product or service based on its consumption of cost-driving activities. This granular approach allows for a detailed explanation of how and why products consume resources and incur costs, enabling businesses to make informed decisions to improve their operations and cost management processes.

In conclusion, ABC is an essential tool for businesses to gain insights into their overhead cost definitions and better understand the relationship between the cost drivers and their impact on the overall business finance. By breaking down key ABC terminologies and employing the methodology in cost management, organizations can obtain accurate data to make well-informed decisions that drive profitability and growth.

Implementing ABC Activity Based Costing in Your Organization

The road to ABC implementation and costing system adaptation begins with identifying the costs in your organization that need to be allocated. To effectively execute an ABC system, the establishment of cost pools becomes necessary. These pools help categorize both secondary costs, serving other parts of the organization, and primary costs, directly related to production.

To allocate costs from secondary pools to primary ones and ultimately to specific cost objects (e.g., products, services), employing activity drivers becomes crucial. This utilization of activity drivers enables businesses to implement targeted overhead reduction strategies and improve their cost management processes.

To further illustrate the practical implementation of ABC in an organization, the following step-by-step process can be a useful guide:

- Identification of all indirect costs that need allocation

- Grouping of these costs into primary and secondary cost pools

- Selection of appropriate activity drivers for each cost pool

- Allocation of secondary costs to primary cost pools using activity drivers

- Further allocation of primary costs to individual cost objects based on activity driver usage

By using this approach to implement ABC within your organization, it will be easier to identify previously unnoticed cost inefficiencies and opportunities for improvement. As businesses continue to evolve and their product offerings expand, adjusting to a more comprehensive and accurate costing system, like ABC, can significantly contribute toward better financial management and informed decision-making.

These examples show how ABC calculations work in a simplified setting. In practice, organizations must apply these formulas across shared services, compelx cost structures, and enterprise-wise allocations.

Our Corporate Cost Allocations whitepaper explains how to apply ABC calculations at scale.

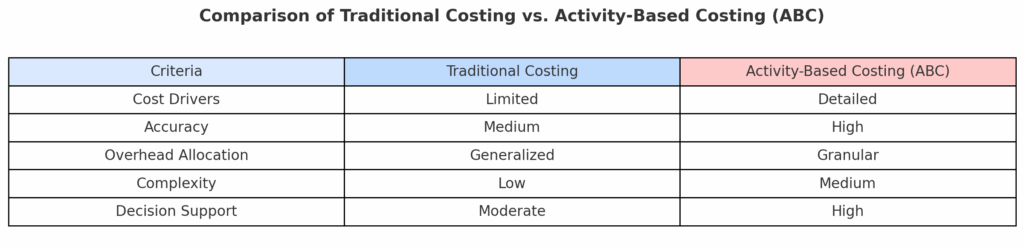

Comparing Traditional Costing with ABC Activity Based Costing

When evaluating costing methods, it’s essential to compare traditional costing approaches with ABC costing to understand their differences and impact on product cost accuracy. Traditional costing methods often fall short in capturing the intricacies of various cost-generating activities, particularly in diverse and complex manufacturing environments.

Distinguishing between Traditional and ABC Costing Approaches

Traditional costing methods are typically based on volume, such as direct labor hours, and allocate overhead costs uniformly across products. This simplistic approach can lead to inaccuracies, especially in organizations with a wide range of products consuming resources at different rates. On the other hand, ABC costing focuses on tracing costs back to the root activities driving them and employs a more detailed, activity-focused approach. This enables companies to allocate overhead costs more accurately to the products consuming the resources.

Case Studies: The Successes of ABC Over Traditional Methods

Real-world case studies and cost analysis comparisons have demonstrated the advantages of ABC over traditional costing methods. By delivering more precise product cost information, ABC has allowed businesses to form informed pricing strategies while better identifying margin-rich products or services. Such insights result in overall improved cost management and strategic decision-making.

- Company A: A manufacturing company experienced a significant increase in the accuracy of product costs after implementing an ABC costing system. This led to more informed pricing decisions and the identification of high-margin products, resulting in higher profitability.

- Company B: A service provider utilized ABC costing to uncover hidden costs in their service offerings and reallocate resources more effectively. By focusing on high-value activities and reducing resource waste, the company improved its cost management and increased overall efficiency.

In conclusion, companies that have adopted ABC costing methods have seen marked improvements in product cost accuracy and cost analysis comparisons, leading to better-informed pricing strategies and resource allocation decisions. As a result, organizations using ABC methods can achieve a competitive advantage over those still relying on traditional costing approaches.

Conclusion

In today’s competitive business landscape, adopting a comprehensive financial strategy is crucial for driving cost effectiveness and making informed decisions. Implementing the Activity-Based Costing (ABC) methodology is a testament to a company’s commitment to utilizing data-driven insights and business analytics to optimize their operations. ABC offers a granular analysis of cost structures, enabling companies to gain a better understanding of the causal relationships between costs, activities, and final outputs.

The advantages of utilizing ABC are evident in the realms of pricing accuracy and overhead management, which are essential aspects of a holistic approach to financial strategy. By accurately determining the costs associated with each activity, organizations can achieve greater levels of resource allocation precision and create a competitive advantage. However, the implementation challenges should not be underestimated, as they require careful consideration and planning to ensure the successful application of this methodology.

In conclusion, the ABC methodology is a highly effective tool that can lead organizations toward increased profitability and deeper insight into their cost structures. With a thorough understanding of this approach, businesses can maximize cost effectiveness, align their financial strategies with their goals, and improve their overall performance in an ever-changing economic environment.

FAQ

What is Activity-Based Costing (ABC)?

Activity-Based Costing (ABC) is an accounting process that assigns overhead and indirect costs to specific products and services by focusing on the causal relationships between costs, activities, and final outputs. This approach aims to achieve accuracy in cost data, resulting in true costs, particularly for companies with complex production processes.

How does ABC differ from traditional costing methods?

Traditional costing methods allocate overhead costs based on production volume and do not capture the underlying complexity of various cost-generating activities. In contrast, ABC provides a more detailed and activity-focused approach, allowing companies to trace costs back to the factors that truly drive them and allowing them to form more informed pricing strategies.

What are cost drivers and cost pools in ABC?

Cost drivers are the factors that create costs, such as machine setups or quality inspections, while cost pools are groupings of individual costs related to specific activities. In the ABC methodology, the cost driver rate is calculated by relating total overhead costs to the number of occurrences of the cost driving activity, providing a granular approach to cost allocation.

What impact does ABC have on pricing and business strategy?

ABC greatly influences business strategy, particularly in pricing strategy formulation. By providing an accurate depiction of product costs, companies can set prices that reflect true value and resource allocation, potentially offering a competitive advantage. The granularity of the cost details obtained through ABC allows for a strategic analysis of cost pools and cost drivers, shaping decisions that can lead to more profitable pricing strategies and enhanced understanding of operational efficiencies.

What are some advantages and challenges of implementing ABC?

One of the main benefits of ABC is the increased accuracy in the allocation of indirect costs, offering a refined approach to assigning overheads via an expanded number of cost pools and new bases for cost allocation. However, challenges may arise, such as the complexity inherent in implementing and maintaining the system and the potential for inaccuracies if cost drivers are not correctly identified or applied.

How can an organization implement ABC?

Implementing ABC requires identifying the costs to be allocated and setting up cost pools that reflect secondary costs (serving other parts of the company) and primary costs (more closely aligned with production). Utilizing activity drivers, costs from secondary pools are allocated to primary pools and then to specific cost objects—such as products or services. This process can enable targeted overhead reduction strategies and more deliberate and effective financial management within an organization.

Source Links

- https://www.accountingcoach.com/activity-based-costing/explanation

- https://www.investopedia.com/terms/a/abc.asp

- https://www.accountingtools.com/articles/activity-based-costing

If you’d like to learn how time equations and capacity cost rates can reduce ABC maintenance, you’ll find Time-Driven Activity-Based Costing (TDABC) useful. To explore the ABC solution further, request a demo.