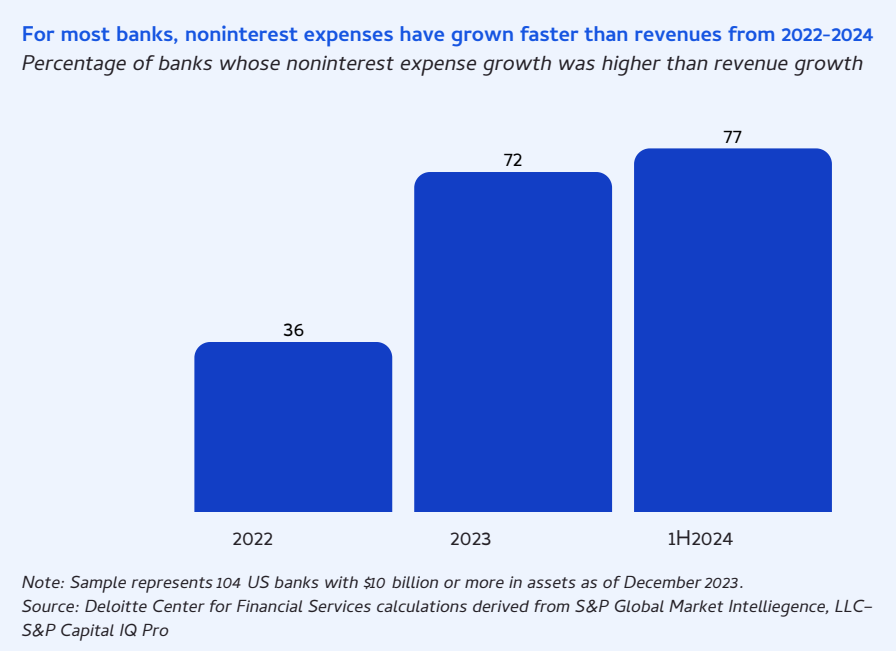

In today’s margin-compressed banking environment, cost optimization can no longer rely on one-off cuts to protect cost-to-income ratio. The relief is temporary. Within 12 to 18 months, the cost base rebuilds and you are back in front of the board explaining why profitability has not structurally improved (McKinsey).

The risk is not cost creep alone. It is cutting into the muscle that protects margin: critical talent, risk infrastructure, and digital investments. Reducing spend is easy under pressure. Redesigning the cost structure without weakening capital flexibility, competitive position, or regulatory standing is far harder.

Leading banks are shifting from one-off cuts to structural cost redesign. Activity-based costing in banking across product, segment, and channel reveals where margin is destroyed, which products fail to earn their cost of equity, and where cost-to-serve erodes returns.

“Cost optimization is not about spending less. It’s about allocating every dollar to the activities that protect ROE under margin pressure.” – Sander Den Hartog, CEO at CostPerform

The approach structurally improves efficiency ratio, strengthens profitability, and creates capital headroom to fund AI and digital modernization without recurring cost-cutting programs. To stay ahead of cost pressures, banks are building strategic cost management programs around two core principles:

Principle 1: Identify Cost Improvement Opportunities Now

Start with rigorous cost transparency. Bank executives audit cost structures to expose hidden ‘bad costs’, such as manual work, redundant controls, fragmented systems, and products with poor cost-to-serve economics. Cost transparency reveals not only where capital flows, but why. Without it, Finance cannot credibly answer the board’s most difficult profitability questions.

In 2026, US banks are prioritizing 5 key cost optimization initiatives:

1. Branch and footprint drilldown

Many North American banks continue operating at cost-to-income ratios around 60%. Overlapping branches and underused real estate inflate noninterest expense without sufficient return. Regional banks that expanded pre-COVID now face the reality of excess footprint.

Granular profitability analysis allows you to assess branch economics by segment and market, supporting data-backed consolidation decisions. The benefit is immediate: efficiency ratio improvement within reporting cycles, capital freed for reinvestment, and footprint optimization without compromising client coverage or regulatory commitments.

2. Automation, cloud computing, and AI

Modernizing back-office operations with RPA, machine learning, and agentic AI removes manual reconciliations and legacy inefficiencies that inflate OPEX. Reporting, loan processing, and onboarding become faster and less labor-intensive. More than 50% of bank executives are investing in Generative AI and 38% expect operating cost reductions. The opportunity is lower run-the-bank expense, and better visibility into profitability by product and channel.

There is real financial risk. If you automate before simplifying, you hardwire broken processes into your operating model and future cost base. Simplify and reengineer before you digitize. Do not automate complexity.

3. Process improvement and understanding demand

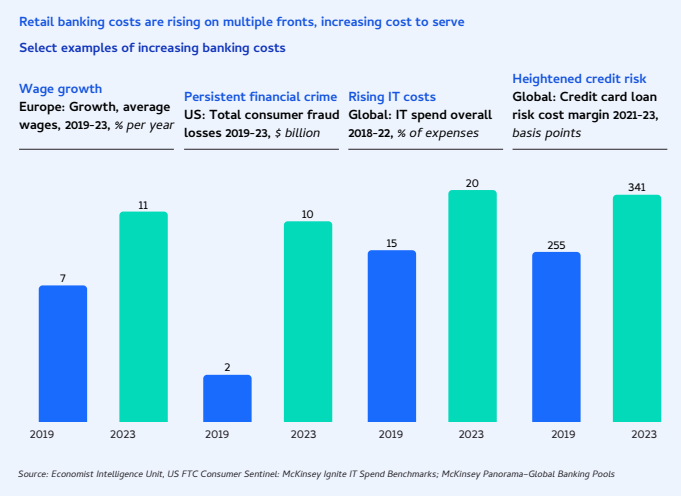

Manual procedures have survived for years despite offering zero ROI. Mortgage origination costs doubled from roughly $5,100 in 2012 to $11,600 in 2023 due to layered compliance and bolt-on systems. In response to rising costs, banks typically focus on quick budget cuts within mortgage operations. These typically include measures such as reducing staffing in processing or underwriting teams, limiting vendor spending, postponing technology upgrades, or tightening departmental budgets.

A strategic approach asks, “Should this activity exist at all?” Exiting sub-scale product lines, eliminating low-value processes, or redesigning workflows can deliver more durable cost takeout. The objective is to protect margins without weakening client experience or regulatory standing, the trade-off every CFO fears.

4. Third-party spending and procurement

Non-labor cost rationalization prevents capital leakage. Banks carefully review vendor contracts, software licenses, marketing, and travel. By consolidating suppliers, leveraging scale purchasing, or joining consortia, banks strengthen negotiating power, lower structural OPEX, and improve earnings predictability without reducing frontline capacity or constraining growth investment.

US banks are mirroring UK peers by tightening discretionary spending, including employee travel and entertainment, while protecting revenue-enabling capabilities. Aim to structurally lower noninterest expense, not another temporary cost program.

5. Organization and workforce efficiency

Labor is the largest expense for most banks. Structural efficiency requires thoughtful workforce restructuring, not across-the-board cuts.

Following its merger, Truist Bank consolidated businesses, closed redundant branches, and streamlined headcount to improve operating leverage, resulting in $750M in cost savings. Leading US banks use attrition, selective redundancies, reskilling, while smaller banks rely on outsourcing, and shared infrastructure (e.g., payments platforms) to benefit from scale. When executed together, these actions can deliver 3-5% structural cost reduction, and up to 10% for top performers, with savings sustained through recurring cost discipline rather than one-off programs.

Principle 2: Build a System of Ongoing Cost Control

As highlighted earlier by McKinsey, short-term savings don’t last without strong governance. Sustainable efficiency requires structural governance.

CFO-Led Performance Management

Cost accountability must cascade through the organization. Clear cost targets by business unit, aligned to enterprise-wide efficiency goals, create ownership. Several banks tie management compensation to cost objectives, balanced with customer service and risk metrics to avoid unsafe cuts. Performance reviews must address expense variances with the same rigor as revenue shortfalls. Ultimately, the CFO must drive a “performance-oriented culture” where teams manage cost and profitability together.

Zero-based budgeting (ZBB) and Cost Ownership

Incremental budgeting institutionalizes inefficiency. ZBB forces departments to justify spend from zero, challenging legacy systems, redundant applications, and underperforming initiatives before they quietly dilute ROE. This approach reduces institutionalized waste and aligns spending with forward strategy.

Continuous Monitoring and Cost Governance

Updated cost models must reflect product changes, system upgrades, and organizational shifts, otherwise cost creep quietly rebuilds before the next board review. Managers must understand how operational decisions impact the efficiency ratio. When accountability extends beyond Finance into frontline leadership, savings hold and margin remains defensible under scrutiny.

The principle is straightforward: economic truth over accounting convenience. Transparency enables accountability, and accountability protects margin.

What’s at stake?

Even a 5% improvement strengthens ROE, frees capital for AI, and puts you back in control of your margin, while competitors remain trapped in recurring cost programs.

Bring the plan to action by structurally lowering your efficiency ratio. The US average sits around 58-60%, leading Nordic banks operate closer to ~42%, and closing that gap could unlock up to $200 billion in industry-wide savings between 2026 and 2028. For more on this, read the Cost Optimization in Banking Playbook.