NIM is a critical metric in banking. It stands for Net Interest Margin, the gap between how much a bank earns from its lending and what it pays on deposits.

In this article, we’ll describe at a high level how a bank calculates its NIM, both the formula used and the process & technology that most banks have in place to support the calculations.

You may also be interested in our other articles in this series, where we cover topics like zero-based budgeting and Fund Transfer Pricing for banks.

The Formula to Calculate NIM

Banks earn interest from loans they provide (mortgages, business loans, etc.). Banks then pay interest on deposits (savings accounts, term deposits, current accounts).

NIM is the spread between those two.

Practical Example: How to Calculate NIM

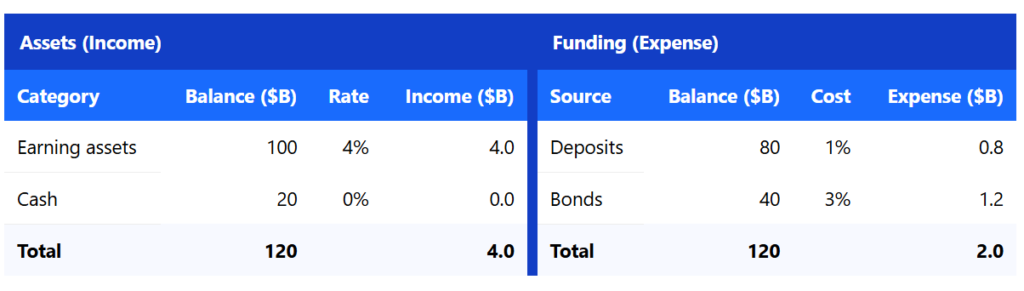

Below is a simple example showing how a bank generates interest income from assets and incurs interest expense from its funding mix, resulting in Net Interest Margin.

In this example, we assume the bank has an asset mix of assets (earning 4% interest) and cash (earning no interest), while on the funding side, the bank has customer deposits (paying 1% interest), and bonds (3%).

NIM Calculation

Interest Income: $4.0B

Interest Expense: $2.0B

Net Interest Income: $4.0B – $2.0B = $2.0B

NIM = 2.0 / 120 = 1.67%

Explanation of the Calculation

Once the total interest income and expense are calculated, the difference between the two (in dollar terms) gives Net Interest Income.

Finally, NIM is calculated by dividing this difference by the total interest-earning assets, giving the result of 1.67%, or 167 basis points.

Why Bank Executives Calculate NIM

For executives, NIM is a critical profitability metric. As with Net Profit Margin at a company manufacturing goods, a high NIM is a key indicator that the bank is earning significant profits relative to its size.

Key Drivers of NIM

What are the drivers of NIM at a bank? There are a few core levers that influence the profitability of a bank, including the interest rates on each side of the balance sheet, and the funding.

Deposit Interest Rate

The interest rate paid out by the bank on deposits is a huge influence on a banks NIM rate offered to savers or clients who leave money on deposit is of critical importance. If these rates are changed, the NIM can shift quickly.

Lending Interest Rate

The rate of interest paid to the bank on its lending (like mortgages) is also a major driver of NIM. The rate secured by the bank on mortgages and other loans will directly impact overall returns.

Funding Mix

The breakdown of assets and liabilities that comprise each side of the balance sheet also affects the calculation of NIM. Is funding 70% deposits and 30% capital market bonds? A shift of this mix from capital market funding to deposit-based funding, they would see the NIM change considerably. As you saw in our earlier example, the interest rates of each component can differ substantially.

Why Break Down NIM?

Breaking down NIM, isolating core drivers or determining the impact of an asset type on the calculation, is a particularly useful exercise. It is not just a calculation to reach a final figure, but a holistic exercise.

The treasury of a bank may find value in identifying strengths and weak spots within the balance sheet. This helps highlight areas that can be optimized to improve profitability.

Why NIM Matters in Banking

It’s a critical measure of profitability. Banks can capture enormous market share, but like any large company, it is possible to control significant volume while failing to generate strong profits.

NIM is a key metric for shareholders, executives, and CFOs to monitor in order to maximize profitability. A focus on Net Interest Margin is a focus on both quality and quantity of earnings.

Process & Technology to support NIM calculations for banks

When decision makers at a top bank like JPMorgan gather to chart their course for the period to come, a strong foundation of data is absolutely critical in making the right choices. Any discrepancy is unacceptable when amplified by the scale of trillions of dollars of assets, or hundreds of billions of dollars of revenue.

IT provides is the basis of all this data. Banks use proprietary systems supported by mass-market solutions. Asset-Liability Management provided by Oracle, cost allocation in banking tools like CostPerform, and data warehousing infrastructure all combine as critical building blocks in the technological machine that supports these decisions.