The Imbalance of Infrastructure and Value in Telecoms

New technologies can create new value, but that may always come at a cost to incumbents. Telecom operators across Europe and the United States continue to face new pressure from new technologies and transmission methods. In the 2000’s, we saw broadcast media continue its convergence with the telecom infrastructure.

In 2025, Operators face the challenge of continued incursions on their infrastructure by “free-riding” media like Meta, Netflix, and ChatGPT, who provide zero capital investment yet create endless value from their services. Other trends such as app-generated media in the Middle East, Africa, and Southeast Asia show a continuously evolving relationship between telco’s and media. While the threat of broadcast media posed similar threats decades ago, merging with hi-tech companies is increasingly difficult for legacy operators.

Erosion of Platforms and Infrastructure

Landlines and fax machines, two technologies which a few decades ago were likely to be found in every home or office, are now close to being extinct. A few notable exceptions aside, like Japan’s now infamous low-tech bureaucracy, fax, and landline have seen their usage fall to near zero. Could fiber broadband face the same issues sooner than expected? While unlikely, there are some early fears that fiber usage may face the same fate sooner than expected. See our 4 predictions for how 5G, 6G, and satellite might reshape fixed line demand.

Outside the home, applications like autonomous vehicles depend on near-instantaneous communication with edge servers and other vehicles, often via 5G radio access networks, to make split-second decisions. If consumers are willing to trust 5G reliability to drive them home, they’ll be confident enough to use it to make work video calls.

Or, as more devices in both domestic and industrial environments become connected, will the need for ultra-reliable, low-latency connectivity be critical, not just desirable. In the home, this includes smart care support devices such as fall detectors, remote health monitors, and emergency response systems for elderly or vulnerable individuals, which rely on real-time data transmission to function safely.

Even seemingly mundane household appliances, like smart ovens, fridges, or heating systems, are increasingly connected to cloud platforms for remote control, predictive maintenance, and energy optimization. As these devices shift from convenience-based to mission-critical roles, consistent and low-latency connectivity becomes non-negotiable. Reliability may become more critical than pricing, but will that be enough to sustain take up of fixed line networks?

Difficulties Ahead in Fiber?

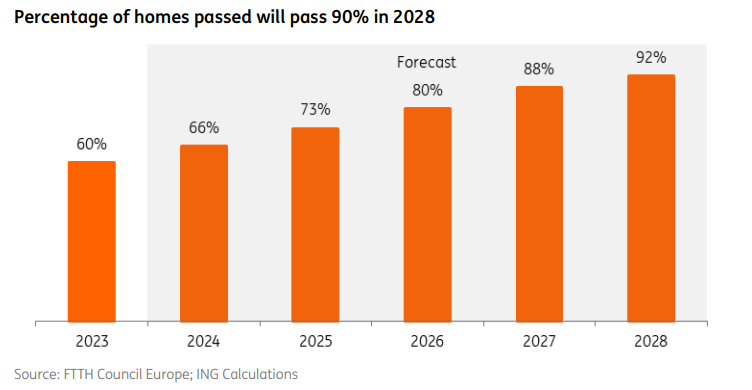

Competition from the likes of Starlink, mobile internet, and slow uptake remain pressing concerns for fiber globally. Fiber rollout across Europe is progressing swiftly, but disappointing household uptake is identified as one of the most important challenges in the years to come. Belgium, Czechia, and Greece stand out as laggards, but fibre penetration rates in the EU27 and UK are expected to pass 90% in 2028.

But while the rollout progresses, the take-up on new fibre connections is a struggle. Some existing connections churn, while new take-up is slow. Some customers are happy with existing technologies like xDSL and coax, while the threats of cheap and fast 5G, 6G on the horizon, and investments in satellite technology by American giants Amazon and Starlink looms around the corner.

Full-Fibre investment business cases are predicated on being able to upsell customers to higher speed products over the long term. Many companies have incentivised customers, either through rental-free periods or discounting, to encourage switches to new speeds in the hope that they don’t go back. It’s essential for organizations to use scenario analysis tools to make the right decisions (which customers, what discount value and length) to ensure network investment provides long run returns on these complex matters.

Where to Focus Fiber and 5G roll out?

Telcos in the middle of major infrastructure roll out (full-fibre, 5G, or soon to come 6G) face choices between when to invest in specific geographical regions, or whether to invest in regions at all. Urban locations typically provide the lowest unit costs for telco network operators due to the economies of scale from covering many more end users over a small location (e.g. in estates of large multi-dwelling units like tower blocks) and higher take up.

Rural locations often require negotiations with government in order to obtain funding incentives in order to connect remote and expensive citizens. Competition from alternative network providers can be common in both, due to the attractiveness of urban returns or the ability for a smaller provider to specialise in smaller rural areas; Starlink and similar satellite providers offer a compelling option for remote areas, with no increase in infrastructure costs.

Telcos need to be able to run forward-looking scenarios on market share and pricing, reflecting an awareness that any delay building in a geographical market could lose them the first mover advantage. However, acknowledging that 100% coverage may not maximise returns for shareholders.

→ Explore Telecom Cost Management

Costing Chaos: EBITDA and Revenue Mismatch

With these challenges and uncertainties, both ongoing and on the horizon, the landscape for a financial decision maker at a major global Telco has become increasingly difficult to predict. Will a reliable and fast fiber network maintain its value and appeal to customers well into the next decade? Will satellite and mobile towers continue their uptick? The question of where to position your investments becomes harder to pinpoint.

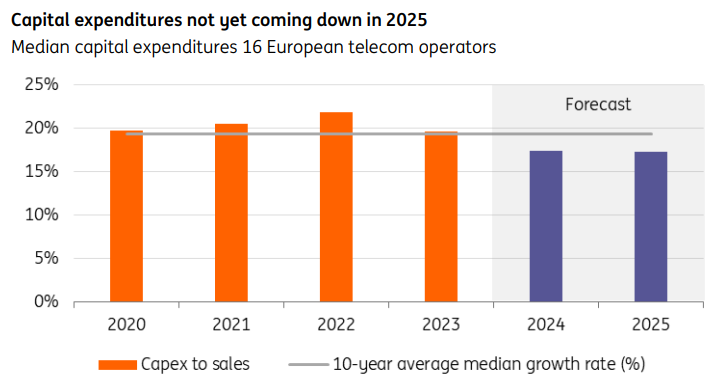

Despite the challenges, no material declines in capital expenditure is forecast. In Europe, inflation and wage growth has largely steadied off in 2025, no doubt contributing to the expectation of healthy EBITDA growth for European Telcos, as wage bills decrease, while AI-bolstered workers increase productivity. But the EBITDA growth comes amidst limited revenue growth, as new opportunities for value generation on the revenue side decrease

The Challenges Ahead

Telcos need to protect their big network investments while also teaming up with the services that use their pipes. By running simple “what-if” models, they can decide where to build fiber or 5G first and which offers lift returns fastest. At the same time, fair cost-sharing deals with Meta, Netflix or other OTTs can help cover upkeep without stifling innovation. In short, success means smart planning, balanced budgets, and open partnerships, so operators remain crucial in a world where value and infrastructure must share the load.

Want to learn more?

Watch our latest webinar on telecom cost optimization or contact us to learn more about building a modern costing framework.